Cable Operators

Ramping on Media and Telecom Part II

“Get off the internet, I need to use the phone!” - Dial-up subscriber in the ‘90s

Welcome to the second part of my Ramping on Media and Telecom series where I explore the different sub-sectors of the industry and write about them. Check out my first article on Local TV Broadcasters and my introductory post explaining the rationale behind this series. In this piece, I’ll delve into cable operators including a little bit of history to understand how the industry developed as well as some of the trends we’re seeing today. As a reminder, these write-ups serve as a primer for those, like me, embarking on an exploration of the sector. While they’re not a pitch for a particular stock or a deep dive into a specific investment topic, it should prepare you to have an intelligent conversation about the sector and prompt questions for further research.

At present, the two largest cable companies by total passings1 are Charter Communications (CHTR) and Comcast (CMCSA), each boasting a footprint encompassing ~40% of total U.S. households. Privately traded Cox Communications has a footprint that covers ~8% of U.S. households while Altice US (ATUS) has ~7% coverage. From there, there is a long tail of regional cable providers that are much smaller including Mediacom (private), Cable One (CABO), WideOpenWest (WOW) and Breezeline (owned by Cogeco in Canada CCA.TO) with roughly 3%/2%/1%/1% coverage respectively.

From the late 1990s to the early 2000s, cable operators underwent a narrative shift - from media companies threatened by the ascent of digital alternatives to being viewed as distribution infrastructure providers capitalizing on the surge in internet usage. Between the late 2000s to the mid-2010s, it became increasingly apparent that cable had clinched victory as the preferred wired infrastructure. Despite the decline of linear TV subs and escalating programming costs, the broadband segment's consistent growth and reduced capital requirements fueled higher ROI. Consequently, cash flow profiles strengthened, ushering in an uptick in capital returns to investors and expanding market multiples. More recently however with subscriber growth stalling and turning negative, investors’ outlook for the sector has shifted dramatically - viewing the cable operators as gradual share losers in a world where fiber is taking share at the high-end and FWA is taking share at the low-end. Just as leveraging fixed costs is a boost on the way up, it’ll hurt pretty badly on the way down. Cable just keeps getting kicked in the teeth these days.

What is cable?

The cable operators build and manage wires, equipment, and other infrastructure that digitally connects users to entertainment, information, and each other for a recurring fee. This includes internet (also referred to as broadband), television (linear or pay TV, also referred to as video), telephone/landlines (also referred to as voice), and mobile services (also referred to as wireless). The industry was borne out of bridging communities of eager viewers with distant TV broadcasting signals in the 1950s before connecting them to a greater variety of paid programming networks in the 1970s. Subsequently, it significantly bolstered its infrastructure capacity, timely meeting the demand for internet connectivity in the mid-90s. More recently, it cautiously entered the realm of wireless offerings through partnerships with incumbent telcos. Along the way, cable has competed with direct broadcast satellite (“DBS”), telephone line operators, wireless providers, and not to mention amongst themselves; all the while navigating 75 years of regulation and deregulation.

The physical assets are primarily the fiber and coaxial cables that make up the operator’s network as well as the facilities that make up the nodes on the network where the signals are received and processed (also called the “headends”). Cable networks utilize a hybrid fiber-coaxial (“HFC”) architecture which means they combine optical fiber and coaxial cables. Coaxial cables conduct electrical signals and typically consist of four layers: a copper wire core enveloped by an insulating material, further encased in a conducting copper shield, all protected within a plastic outer layer. It is a better transmitter of radio frequency signals than many other methods because the electromagnetic field of the signal exists only between the inner core and the conducting copper shield (i.e. between layers one and three) and as a result doesn’t suffer from external interference.2 Optic fiber cables consists of dozens or hundreds of thin3 strands of glass or plastic that transmits data via pulses of light. This inner core is usually wrapped by a layer of glass called cladding, which reflects the light inwards to prevent the loss of signal. Fiber transmits data farther and at higher bandwidths than electric cables. In a typical HFC network, signal is received and processed by the headend and then transmitted across the network in fiber cables before hitting an optical node that takes the light signals and translates it to radio frequency, which is then sent along the coaxial cables that ultimately reach subscribers. For the vast majority of the distance that the signal is traveling, it’s through fiber cables.

See below for a snapshot of the financials and KPIs of some of the publicly traded cable operators based on FY2023 data:

You’ll first notice how much bigger CHTR and CMCSA are vs the rest of the peer group, accounting for ~60M subscribers across their business lines, which accounts for nearly half of all households in the U.S. The business mix is similar across the board (refer to Figure 2. Revenue Breakdown) with roughly 3/4 of revenues coming from residential, 15-20% from commercial, and the remainder being other revenues - the exception is CMCSA with a significantly greater portion of revenues coming from Other as it owns media assets like NBCUniversal and Sky (part of their Content & Experiences business segment). CMCSA’s EBITDA margins of ~31% is also lower than peers for the same reason with the Content & Experiences segment commanding ~16% EBITDA margins. Excluding the media assets, CMCSA’s margins are closer to CHTR’s 40%.

Figure 3 illustrates the NTM EV/EBITDA of the cable operators spanning the last two decades. With the exception of WOW, CMCSA has consistently traded at a discount to peers, largely attributed to its diversification into media assets. Cable is a steadier business with declining capital intensity, which lends itself to having greater leverage capacity for optimal equity returns. Conversely, media is perceived as necessitating increased investment to contend with streaming rivals and escalating customer acquisition expenses so the combined entity is seen as having an inefficient capital structure as evidenced in its 2.4x net leverage ratio vs pure-play peers around ~4.0x. This type of structure lends itself to a SOTP thesis, although there's no apparent indication of imminent corporate action on this front.

Looking at just the residential segment (Figure 4), it’s clear that broadband is the dominant offering and that it drives the narrative of the business. Pay TV (“video”), while still substantial, is now less than half of the business for the publicly traded cable operators and it continues to shrink over time. While video continues to contribute positive EBITDA, margins are lower than broadband so as video decreases as a percentage of total residential revenues, we should expect overall margins to expand. CABO’s higher mix of broadband vs video and its higher than average broadband ARPU account for its higher than peers margin profile.

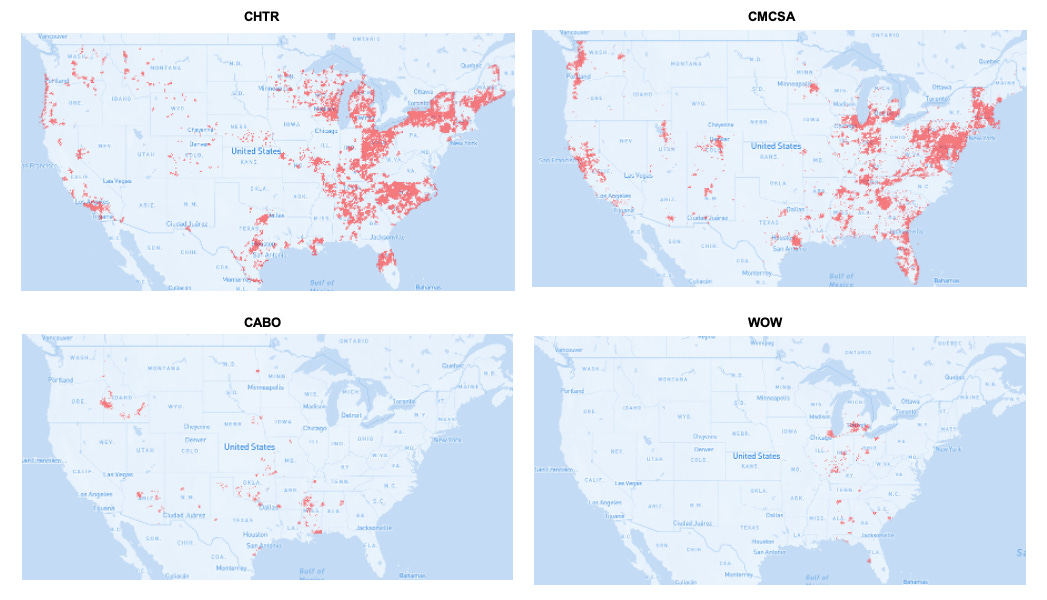

Figure 5 below illustrates the footprint of the cable operators.4 You will notice that the overlap between the operators is minimal. This is because as cable operators were laying down the infrastructure, there were simply more greenfield opportunities to build into than to compete in an already occupied area. As a result, investors historically viewed cable as a better business than telcos because cable operators see less competition in the areas they serve whereas telcos have three, and in the recent past four, players to compete with nationwide. When it comes to the fiber competitors, you’ll hear the term “fiber overbuilder”, which refers to fiber players who are building a completely new network in an area already served by another (typically cable) player, thereby introducing greater competition in the region. While hard to see in the footprint map below, WOW is primarily an overbuilder in both cable as well fiber on the edges - this more competitive dynamics in its local markets explain its lower broadband ARPU of $60/month and the lower multiple that it trades at vs peers.

A brief corporate history

Origins

Most sources pinpoint 1948 as the inception year of the cable industry in the United States, marked by the establishment of cable systems in rural areas of Arkansas, Oregon, and Pennsylvania.. In those areas over-the-air broadcast TV signals weren’t very good, especially if you lived in a valley and there were hilly terrains between your rabbit-ear antenna and the broadcast station. To resolve this, entrepreneurial individuals decided to put up antennas in high elevations like on top of a hill where TV broadcast signals were better and then used a wire5 to transmit the signal down to the community. At the time, these were called Community Antenna Television or “CATV”, a term that we still use today to refer to cable TV system that distinguishes it from over-the-air broadcast (see my post on Local TV Broadcasters for more on that sub-sector). Several individuals are credited with establishing the “first” cable system, though records are inconclusive. One of them is John Walson who began as a TV and radio appliance salesman in Mahanoy City, PA and who famously began his system as a way to bring better TV reception to town and thereby help sell his TV sets. This system, through years of expansion and acquisition, is now the privately-owned group of affiliate systems called Service Electric6, which serves eastern PA and parts of western NJ and is still run by the Walson family today. In 2020 one of the affiliates, Service Electric Cable TV of New Jersey, was sold to ATUS for roughly $150m. Other claimants to being first include Ed Parson of Oregon who at the time charged a $125 one-time installation fee and a $3 monthly subscription ($1,600 and $40 today adjusted for inflation respectively) as well as James Davidson of Arkansas who ran a local movie theater.

Due to the novelty and increasing demand for broadcast TV after WWII a lot of TV station licenses were granted, causing signal interference in many locations. As a result, the FCC put a temporary freeze on awarding new TV broadcast station licenses.7 This ban was originally intended to last six months while the commission figured out the standards that were needed to be put into place. Six months turned into four years, which turned out to be a great opportunity for cable systems to step in to service the rising demand for TV with total subscribers reaching 14,000 across 70 different cable systems by 1952. In 1953, a CATV system in Casper, WY was the first to use microwave relay systems that allowed it to carry signals from long distances, allowing cable to provide previously unaccessible programming from other cities. Unsurprisingly, this seriously pissed off local broadcasters who began to lobby the FCC to regulate cable, thus beginning waves of regulatory and deregulatory agenda throughout the second half of the 20th century. Initially the regulators were reluctant (or more accurately unable) to impose restrictions on cable since they technically didn’t use the public airwaves so the agency did not have jurisdiction over their activities; this view was cemented in the 1956 landmark opinion by the FCC in Frontier Broadcasting v. Collier, which noted that cable systems did not have common carrier status.8 Cable subscribers continued to grow rapidly through the late 1950s and early 1960s hitting over 850,000 customers across 800 cable systems by 1962. That year, the regulatory landscape shifted when the FCC changed its mind and decided that CATV systems were indeed under its regulatory ambit, thereby restricting the use of microwave relays. What is interesting was that this decision was based on the idea that there could be “potential” economic impact to the broadcasters as opposed to showing actual economic damages. The following year in Carter Mountain Transmission Corp v. FCC the U.S. Court of Appeals affirmed this “potential” economic impact argument, curbing cable expansion throughout the remainder of the decade.9 The regulatory attitude shifted again in 1970s as the FCC began to deregulate cable by first loosening programming rules in 1974 before repealing the restriction on importing long distant signals in 1976.

During this early period, several major cable corporations began to emerge. We can’t go far into the history of cable before mentioning the industry pioneer John Malone who ran Tele-Communications, Inc. (“TCI” and publicly traded as TCOMA on NASDAQ until the 1990s). TCI was started by Bob Magness when he merged Western Microwave, Inc. and Community Television, Inc in 1968 before going public in 1970. At that time, it was the 10th largest cable company in the U.S. Magness hired Malone, who went on to grow TCI into the largest cable operator in the country by 1981 and pioneered the focus on levered cash-flow growth through high debt loads to offset taxes instead of maximizing accounting earnings. TCI stock grew at a 30% annual compounded rate under Malone, handily outpacing both the cable industry average and the S&P 500 during that time.10 For those interested in learning more about the history of TCI, I would recommend Mark Robichaux’s book Cable Cowboy or Chapter 4 of The Outsiders by William Thorndike, both of which extensively examine Malone’s legacy at the company. Following a failed merger with Bell Atlantic in 1993, TCI was acquired by AT&T in 1999, forming AT&T Broadband and Internet Services, which was later sold to Comcast in 2002 A subset of TCI’s cable systems in NJ and NY were sold to Cablevision in 1997 while parts of the system in CA, eastern OR, northern Utah, and southern Idaho were swapped to Cable One in 2001.

“I used to go to shareholder meetings and someone would ask about earnings, and I’d say, ‘I think you’re in the wrong meeting’. That’s the wrong metric. In fact, in the cable industry, if you start generating earnings that means you’ve stopped growing and the government is now participating in what otherwise should be your growth metric.” - John Malone

Other notable corporations include TelePrompTer, which began life in 1950 telling the eponymous teleprompter (the thing that scrolls text for people giving speeches) before selling that business and investing in cable and satellite broadcast services. In 1970, TelePrompTer merged with H&B American Corp to create the largest cable company at the time. The company was later merged into Westinghouse’s broadcasting business and renamed Group W Cable, which itself would be mostly sold to Houston Industries in 1986 with a remaining ~25% going to Comcast. Houston Industries renamed the division Paragon Cable and sold it to Time Warner Cable in 1999 with the exception of assets in Florida, which were spun into a new company called Bright House Networks. All of that came back under one roof in 2016 when Charter acquired both Time Warner Cable ($78.1B) and Bright House Networks ($10.4B) to create a cable giant with 24M subscribers.11

Cox Communications, Inc. was also born during this time when Cox Enterprises purchased a number of cable systems in PA in 1962 followed by systems in CA, OR, and WA. In 1998, Cox became the first of the large operators to offer telecommunication services to businesses and in 1997 it became the first to offer telephony services over cable wires. The company went public in 1964 before being taken private by Cox Enterprises in 1985. In 1995 with its acquisition of Times-Mirror’s cable properties, it went public again. As a public company my impression is that Cox was considered by investors to be the best managed cable operator and thus traded at a premium vs peers for a number of years. Customer satisfaction was the highest amongst MSOs in the late 90s and early 2000s and the company’s footprint in high growth second tier markets shielded it from local cable competition for the most part. The company was taken private by the Cox family for the second time in 2005.

Pay TV

The 1970s was also the decade when premium programming began with the first paid programming produced by HBO (rolled out by Charles Dolan and Gerald Levin in 1972). Up until then, cable companies only retransmitted broadcast programming and charged a monthly fee for the connection - now it could produce or purchase it’s own unique premium programming and charge separately. In 1973, the FCC sanctioned the deployment of communication satellites for cable program distribution. Subsequently, in 1975, HBO initiated satellite distribution of programming to cable systems in FL and MI. From the late 1970s through the 1980s, demand for cable TV continued to grow rapidly and we saw the launch of many of the major networks we know today including USA Network (1977) ESPN (1979), CNN (1980), MTV (1981), the Disney Channel (1983), and AMC (1984). The Cable Communications Policy Act of 1984 further deregulated the industry and promoted competition by providing for franchise renewals, deregulating basic rates12, as well as providing investments in programming development. During the 1980s and 1990s cable technology continued to advance with the development of multi-channel, VSB/AM transmission through optical fiber, which became core to the now ubiquitous HFC network architecture by providing greater reliability and higher capacity at an affordable price. Upgrades and rebuilds gradually increased the channel capacity of cable networks as well. Between 1984 and 1992, the cable industry spent over $15 billion in program development and infrastructure investment.13 During this time, the industry began to mature and consolidation stepped up. Direct-broadcast-satellite (“DBS”) became a fierce competitor having been introduced in 1994 to obtaining 13% penetration of all U.S. households by 1999 and 22% by 2004.14 The Cable Television Consumer Protection and Competition Act of 1992 tilted the pendulum back towards heavy regulation by allowing local government to have greater control over cable pricing before the Telecommunications Act of 1996 brought back a more deregulated agenda by allowing cables companies and phone companies to offer overlapping services.15 During this period of growth from 1973 to 1998, shares of publicly traded cable companies compounded at ~20% annually compared to ~14% for the S&P 500.16

Notable players that emerged during this include Cable One, Mediacom, WideOpenWest (d.b.a as WOW!), and Cablevision (previously publicly traded under the ticker CVC). Cable One operates under the Sparklight brand and began in 1986 as a subsidiary of the newspaper giant, Graham Holdings Company before changing its name to Cable One in 1997. It was spun out of Graham and began life as a separate publicly traded entity in 2015. Mediacom is today the fifth largest cable operator in the US and was founded in 1995 concentrating on customers in the Midwest and Southeast. WideOpenWest started in 1996 in Denver and grew through a series of acquisition including Americast in 2001, Broadstripe in 2011, Knology in 2012, and NuLink in 2016. It sold its Cleveland and Columbus systems to Atlantic Broadband in 2021 for $1.125B, which itself spun out of Charter in 2004 and acquired by Cogeco in 2012. Cablevision was founded by Charles Dolan after he sold HBO and its accompanying cable system (Sterling Manhattan Cable) to a company that eventually became Time Warner Cable and named it CableVision to serve the Long Island suburbs. It expanded through the 1980s to systems in Chicago, Boston, and Cleveland and acquired 10 cable systems from TCI to service areas in NY and NJ. In 2010, Cablevision acquired Bresnan Communications (which was rebranded as Optimum West) for $1.4B before selling it to Charter for $1.6B in 2013. In 2016, Cablevision was acquired for $17.7B by Altice, the European telecom conglomerate and merged with the assets of Suddenlink, which Altice acquired a year prior to form Altice USA.

The Telecommunications Act of 1996 also allowed new entrants into the cable industry and existing corporations to operate across market sectors. This spurred AT&T, the 800-pound telecommunications gorilla, to enter the cable market as well as Microsoft’s $1B investment in Comcast. Separately Paul Allen, cofounder of Microsoft, bought a controlling interest in Charter, which at the time was a medium sized cable system based in Missouri and went on an acquisition spree including the $2.8B acquisition of Marcus Cable in 1998 and 10 acquisitions in 1999, the year it IPO-ed.17 These were good times for cable stocks as cash flow growth accelerated and private equity investor including Carlyle, Keystone, and Blackstone poured money into the sector.

Broadband

The 1990s also witnessed the widespread availability of the internet to households for the first time. Initially dial-up was the most available connection as it required only a telephone line to connect to an internet service provider (“ISP”). Early ISPs include The World18, CompuServe, The Source, and AOL. The first commercial dial-up internet access was offered by Sprint in 1992 as SprintLink. Eventually dial-up reaching as much as 40% of American in the early 2000s. As the web took off however, the capacity required web browsing fully used up the telephone lines, resulting in the all too familiar situation where a household is unable to make phone calls and surf the web at the same time. At 56kbps, dial-up speeds were painfully slow for downloading anything other than pain text. Digital-subscriber-line (“DSL”) was developed to offer faster internet connection by carrying digital signals through existing telephone lines. By the mid-90s, cable companies realized that it had been half a century since the first cable wires were built and began a massive wave of capital investments to upgrade distribution networks with fiber optics and coaxial cables - from 1996 to 2000, the industry spent over $36B upgrading its infrastructure to increase broadband services. It turns out that the cable infrastructure was perfectly suited to broadband services given the higher bandwidth that cable was building for vs just voice data that traditionally travelled on copper telephone lines. Broadband allowed for greater capacity, provided multi-channel video offerings, two-way voice and high speed-internet access all through just one wired connection.

Cord-cutting

With the expansion of broadband capacity and the increased ubiquity of internet access, digital video offerings emerged as competitors to traditional cable TV. Cord-cutting gained momentum in the late 2000s as streaming alternatives to cable emerged. The trend accelerated during the Great Recession as households reduced discretionary spending, opting for cheaper alternatives to premium pay TV. Amazon Unbox launched in 2006 but only gained in popularity after rebranding to Amazon Video in 2008 while Netflix launched its streaming model in 2007 shortly before Hulu launched in 2008. At the same time, streaming technology were becoming accessible to consumers as well including the launch of Roku in 2002, Apple TV in 2006 and Chromecast in 2013. Pay TV subscribers peaked in 2014 at ~100m households in 2014 or ~80% penetration and have declined to less than 60% today with declines accelerating in recent years due to the pandemic, even after accounting for the increase in digital Pay TV services such as Sling TV, YouTube TV, etc which have grown to ~18m households today vs 700k in 2015.19

Given that it’s been a decade since Pay TV subs peaked, cable investors understand these dynamics quite well and I don’t believe it will serve as continued downside to the stocks. While the linear TV segment (usually presented under Video in company financials) still generates positive EBITDA, growing programming costs and general deleveraging from declining subs continue to pressure segment margins. Investors generally welcome cable deleveraging itself from the pay TV business as it decreases exposure to the declining business and improves the overall margins as broadband margins are higher.

Recent trends

With all that history as context, we’ve now entered a new era for cable operators; one in which cable is stuck between a rock and a hard place. After a big bump in 2020/2021 due to COVID pandemic (greater work-from-home led to greater demand for high capacity cable broadband), subscriber growth has slowed, and for some, it has begun to decline - partly due to the pull forward from the pandemic but also as a result of continued competition from fiber and more recently FWA. This, combined with the April roll-off of the Affordable Connectivity Program (“ACP”), which subsidized low-income cable subscribers, has significantly reduced broadband net addition estimates. Since December 2021, Revenue/EBITDA estimates for FY26 have fallen by (-14.6%)/(-20.3%) for CHTR and (-8.6%)/(-13.8%) for CMCSA while the stock prices have fallen (-58%) and (-22%) respectively as of the time of this writing.

Fiber Competition

As noted above, optic fiber cables are used in the HFC network operated by cable players but in this context, fiber is sometimes called fiber-to-the-home (“FTTH”)20 where the fiber network extends directly into a subscriber’s home. The first large-scale competitor in this space was Fios, offered by Verizon (VZ). Its development can be traced back to 1995 when it was still Bell Atlantic, testing its Stargazer video services, the first commercial video-on-demand product covering approximately 1,000 homes in Virginia. Stargazer was folded into what ultimately became VZ’s early FTTH video offering, which launched in 2005. At the time, the estimated cost to build was ~$1,220 per home and management was criticized for spending so much capital on a product that many believed customers did not need.21 Expansion stopped in 2010 given how expensive it was to continue building out the fiber optic footprint and VZ chose to focus on increasing penetration in areas where it had already built. VZ had originally planned to build out ~18M households locations but after pausing in 2010, it then sold a portion to Frontier (FYBR) in 2015. Currently, the plan is to expand slowly (by +400k/year to +500k/year) to reach approximately 18 million households by 2025. AT&T commenced its fiber ambitions in 2013 and has quickly expanded to +26M locations and plans to hit +30M by 2025. I’m going to stop the overview here before it becomes a whole history-of-fiber run-on section.

For a long time, cable was taking share from telco’s DSL footprint in broadband so telcos fought back by upgrading their wireline network to fiber by replacing the copper-based DSL network with fiber connections. In addition to telcos, there are fiber overbuilders who are building new fiber networks to compete against cable in existing geographies. The fear for cable operators is that before a market is introduced to fiber, cable was the superior offering and at its service level, consumers really only had one choice of technology (i.e. cable’s HFC networks) and since cable footprints don’t really overlap, these operators enjoyed near monopoly status at that service level in markets that they served. Now with FTTH offerings competing in these local markets, cable all of a sudden has a competitor with a better (although some would argue similar) service level eating away at its subscriber base. To be fair, having a single fiber competitor would still be preferable to facing ubiquitous competition from all three wireless providers in all regions.

Fiber is perceived as a premium product, as evidenced by a 2023 consumer research report by the Fiber Broadband Association, demonstrating that consumers view it as offering higher reliability and faster speeds.22 To what extent this is true is debatable as FTTH networks still have to translate the digital signal from light into an electromagnetic signal at the optical network terminal (“ONT”, also commonly known as a fiber box) through an optical interface. In an FTTH setup, the ONT is next to the home whereas in an HFC setup, this happens at a telephone pole so FTTH really just 20 to 40 feet closer.

FWA Competition

While fiber has been a competitor to cable for many years, a new competitive force has emerged in recent years: fixed-wireless-access (“FWA”). FWA is sometimes called 4G or 5G internet and is basically using a mobile network to provide broadband services in one “fixed” location such as your home or office. When VZ began to roll out FWA in 2018/2019, investors was abuzz with fear - the same way that I mentioned how cable was seen as a premium business vs telco because telco has three national competitors, FWA would suddenly introduce those three large wireless behemoths as competitors nationwide. That prospect, if FWA can pull it off, is much scarier than fiber competition in select markets.

But the second thought that investors (or more accurately, cable-bulls) seemed to come to was that this was a ridiculous notion. Home broadband usage is 45-50x more intensive than mobile; you might use 15GB of data per month on mobile but home usage is closer 600-700GB per month and growing double-digits, suggesting growth to nearly 1TB per month by 2028.23 While mobile data consumption is also growing, the delta between the two is massive. It sounds crazy to use spectrum to offer a product that consumes 50x more data but charge less for it. This also isn’t the first time it’s been tried with VZ attempting a residential LTE broadband service in the early 2010s that didn’t quite catch on.24 How we got here this time is that due to the large C-band spectrum auction and the recent 5G upgrades, telcos found that they had excess wireless capacity. Whether or not the ROI was good, it seemed like the thought process was that they already have this excess capacity so any offering would be incremental to the business. However, cable bulls note that at some point in the near future, as mobile and home data usage continues to grow, wireless carriers will have to choose between deploying more capex to densify the network or let FWA users roll off lest they allow FWA usage to disrupt their wireless capacity.

Putting it all together

Figure 7 above25 shows the broadband market exploding in onto the scene in the late 1990s and early 2000s and steadily growing since to hit >90% penetration of U.S. households recently. Cable (the purple line) has dominated the broadband market for most of its history but the recent plateau and slight decline corresponds to the rise of FWA market share gains (the grey line). Telco broadband subscribes started flatlining in 2007 just shy of 40M subs; since then it appears that legacy DSL sub losses have been roughly offset by telco fiber sub gains.

Figure 8 above zooms into the numbers from the last few years. Since 2020, cable market share has fallen from approximately 67% to around 64% but the more jarring framing is that net adds have turned negative and that FWA is now accounting for nearly 100% of net adds.

Other investment topics

The bloodline of cable is subscriber growth; annual subscriber net adds and EV/EBITDA multiples exhibit a >90% correlation. With the maturation of the U.S. broadband market and FWA’s recent uptick in sub gains, cable stocks have puked. As cable multiples fall to be inline with telco multiples, it feels like the question is how bad will it be for cable going forward. Supplementing this long-term question - here are a few investment topics in rapid-fire fashion:

ACP or the Affordable Connectivity Program provided up to $30/month subsidies to low income households for the purchase of broadband services. The program was launched by the FCC on 12/31/21 and stopped accepting new applications and enrollments on 2/7/24 and the last fully funded month was April 2024. The run-off of ACP benefits will have a negative impact on cable subs with CHTR being hit particularly hard as ~17% of its subs base is exposed to ACP. The run-off is likely to result in elevated subs loss this year, increased bad debt expense, as well as a drag on cable’s ability to raise prices over the next few quarters. With this multi-quarter headwind to subs net add, it’s unlikely we dispel the FWA/Fiber share gain narrative this year even if it turns out to be a more favorable competitive equilibrium longer term. Perhaps 2H24 will be kinder to cable as the industry works through ACP-driven churn and investors can look forward to a possible recovery in net adds next year.

Rural footprints have historically not been a big priority for cable given the unfavorable economics of servicing a low density area but recent government programs such as the Broadband Equity Access and Deployment Program (“BEAD”), which provides for $42B in subsidies, and the Rural Digital Opportunity Fund (“RDOF”) has pushed cable operators to build out its rural broadband footprint.

Mobile offering are new to cable operators and are offered to existing cable subscribers as a way to increase retention. VZ signed an MVNO agreement with CMCSA, Time Warner Cable, and Bright House Networks (the latter two being acquired by CHTR in 2016) and presumably charged the cable operators a wholesale price based on an average price per minute or per gigabyte of data used. Some analysts have pointed out that this actually gave the cable MVNO a cost advantage because CMCSA and CHTR have their own ground facilities so in dense urban areas they can offload the traffic to their own infrastructure and in high cost rural areas, they can use VZ’s network - however because the price charged by VZ is probably an average wholesale price, the cable operators can arbitrage this opportunity by using facilities they already own. Funnily enough, this allows cable operators to offer mobile services at a cheaper price than the telcos despite being MVNOs. There’s a bull case involving cable companies providing a dominant mobile offering, becoming the winner of convergence between wired and wireless operators. I think we’re still too early to make a judgement on this but the logic is sound-ish.

The relationship between cable and media continues to evolve as pay TV sub declines have forced media companies to increase what they charge cable operators in the form of higher programming costs. The CHTR-DIS dispute feels like a turning point with cable putting its foot down and standing up against a power media conglomerate with some success.

I’m going to end the write-up here. Learning about cable was a lot of fun and there’s so much more that I didn’t get to cover including a deeper explanation of the technology and how international markets differ in structure from the U.S. As always, please treat these as my preliminary research notes and share it with anyone who might find it interesting or informative. I invite you to share your thoughts and comments as well!

Passings refers to the number of units (usually households or business premises) passed by the cable network in areas where service is offered.

It’s called “coaxial” because the inner copper wire and the outer copper shield (3rd from the center) are on the same axis and share the same center of the circle if you view it from a cross-sectional perspective.

We’re talking 1/10th the thickness of a human hair kind of thin.

Source: https://www.boradbandnow.com. I excluded ATUS since the site is only showing the northeast footprint for some reason and it was cleaner to fit four into the chart.

Initially people used twin-lead wires before coaxial became more popular. On the popular finance/investing podcast, guest speaker legendary media/telco analyst Craig Moffett noted that the popularity of coaxial was due to its excess production during the Korean War.

https://sectv.com/

https://www.mitel.com/articles/history-federal-communications-commission-fcc

https://casetext.com/case/frontier-broadcasting-company-v-fcc

The First Report and Order by the FCC in 1965 set forth a number of restrictions on cable. In 1966 the FCC required all cable systems in the top 100 DMA to obtain FCC approval for importing distant signals via microwave. In 1968 the U.S. Supreme Court upheld the FCC’s jurisdiction over CATV system. In the same year the FCC froze development of cable systems in the top 100 markets. In 1970, the FCC adopts “anti-siphoning” rules to protect broadcast TV programming…and the list goes on.

https://www.shortform.com/blog/tele-communications-inc-history-john-malone/

https://en.wikipedia.org/wiki/TelePrompTer_Corporation

Price paid for the basic cable channels which provides access to broadcast TV networks like ABC, NBC, CBS, Fox, The CW, MyNetworkTV, PBS etc, as well as free or low-cost channels like C-SPAN.

https://seatup.com/blog/history-of-cable/

https://www.nab.org/documents/newsRoom/pdfs/Capacity_Trends_in_DBS_and_Cable_TV_Services.pdf

https://syndeoinstitute.org/wp-content/uploads/2022/10/CableTimelineFall2015.pdf

https://www.shortform.com/blog/tele-communications-inc-history-john-malone/

https://www.seattletimes.com/business/economy/paul-allen-charter-and-what-might-have-been-jon-talton/

Apparently they’re still around: https://www.theworld.com/

https://www.emarketer.com/content/youtube-tv-leads-digital-pay-tv

I’m going to use fiber and FTTH synonymously in this article

https://www.lightreading.com/fttx/verizon-could-be-a-sleeping-giant-in-us-fiber-expansions

https://fiberbroadband.org/wp-content/uploads/2023/08/The-Status-of-U.S.-Broadband-2023.pdf

https://www.cnet.com/home/internet/how-to-manage-your-home-internet-plans-data-cap/

https://www.pcmag.com/archive/verizon-to-challenge-att-comcast-with-fixed-lte-service-289730

https://www.spglobal.com/marketintelligence/en/news-insights/research/the-history-of-us-broadband