Instacart S-1 Analysis Part II

Some discussion on projections, valuation, and more on cohorts GTV

Welcome to Part II of my analysis on CART’s IPO, if you find content like this interesting, please subscribe to this free research journal as I learn and write. See here for Part I of my Instacart S-1 Analysis where I dig into unit economics, retailer fees, and a first look at cohort data.

TL;DR - CART’s coming in cheap at $27/share at the midpoint (at least compared to gig economy peers) but it’s probably because growth has slowed and the (relatively) new management team has focused on profitability, but hey, I thought that’s what the market wanted to see. Grocery grows LSD, delivery probably LDD to mid-teens as it increases penetration. CART probably loses some share to DASH/UBER/AMZN or grocery white-label and there’s minimal room for take rate expansion based on the LT target so transaction revenue is a HSD grower while advertising seems to have much greater room to grow, netting CART out to probably a HSD/LDD revenue grower in the base case. The 2020 cohort is probably a 1-4% headwind to GTV over the next few years and depending on how new cohort behaviors come out, things can go either way. Personally, I’m just not sure I’m willing to pay much of a premium for grocery delivery the same way I will for food delivery. I’d like to know what CART’s next big product will look like and what (if anything) will drive the next leg of growth. Based on the investment positives and negatives, CART’s cheap but because people might perceive it as perpetually a slower grower than the rest of the gig-economy players.

All estimates are my own so if you notice a mistake, please let me know.

More on Cohorts

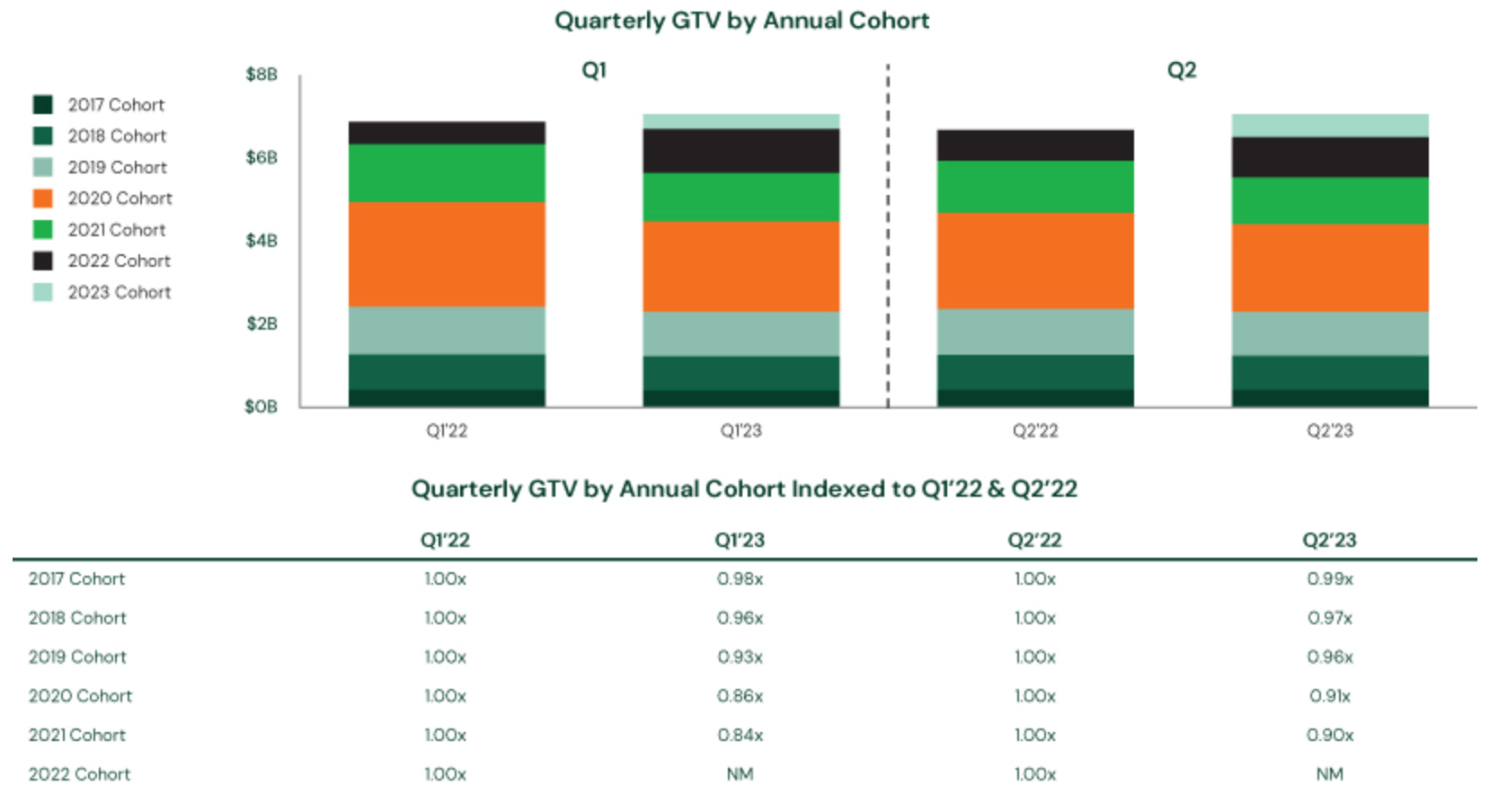

As explained in Part I, my favorite cohort disclosure from the S-1 is the GTV by cohort since it includes the full GTV of the customer cohort who placed their first order in a given year so that the impact of churned customers are accurately reflected in these charts.

Using these charts and a digital ruler, I’ve estimated the dollar amount of GTV associated with each cohort over time. As discussed previously, each cohort experienced a significant boost during COVID but the 2017/2018/2019 cohorts continued to grow total GTV in 2021/2022 while the 2020 cohort saw declines, which isn’t surprising since many in the 2020 cohort were forced to adopt the service due to COVID and readily churned when grocery stores were safely accessible in person again.

Below the cohort GTV and growth % portion, I’ve included CART’s customer acquisition cost (“CAC”), which they break out between customer incentives & promotions (part of contra-revenues) and customer market expenses (part of the S&M expense line). Instead of the usual LTV/CAC analysis or CAC per customer, I’ve calculated in-period GTV/CAC, which is the GTV from a period’s cohort divided by that period’s CAC - basically how much new GTV CART gains from new customers per dollar spent on CAC. Yes, I know incentives and promotions might not necessarily all be for new customers; part of it is reengaging customers that have stopped using the app or increasing engagement of existing customer but since this is what they’ve allocated as customer ‘acquisition’ cost, I’ll treat it as such.

A few things that jump out:

All cohorts excluding the recently acquired 2022 cohort are experiencing YoY declines in GTV in 1H23.

What’s notable is that the GTV declines increase as we go from older cohort to newer (2021 declines > 2020 declines > 2019 declines > 2018 declines).

This is somewhat scary since it is showing that cohort quality has degraded over time.

I would have imagined the 2020 cohort would experience the most declines since many in that cohort are likely returning to in-person grocery shopping but that’s not the case. The 2021 cohort GTV is declining even more currently.

While this trend isn’t totally unexpected since the more hardcore users would have adopted earlier so later adopters are slightly less active, this implies that CART may be hitting up against the customer saturation limit for those that are actually interested in paying up for grocery delivery.

The 1H22 cohort is seeing ~54% YoY increase in GTV, which is quite positive since everyone else is seeing declines. There also seems to be a trend of each cohort seeing a sharp increase in Year 1 post acquisition (hard to be certain because of the weird 2020 dynamic in the middle of historical data) but even so, the 54% year 1 growth for the 1H22 cohort is better than the 29% year 1 growth for the 2021 cohort.

I’m not sure what to call this so I’m going to term it the new cohort year-1 pop.

I’m not entirely sure why this happens (or why this is suppose to happen). My best guess is that this is roughly when an acquired user decides they love the product and increases their usage from once to multiple times per quarter and that meaningfully offsets the churned user who decides they don’t need this, so you see a pop in year 1 and then growth steadies for the cohort.EDIT: this is due to users only contributing only a partial year in the year they are acquired whereas year 1 is the full year. Nothing magical going on.

In-period GTV/CAC spiked in 2020 and has been declining. 1H23 saw this drop sharply to 2.7x from 5.9x in 2022.

The 5.9x in 2022 was 4.6x in 1H22 and 7.2x in 2H22. My sense is perhaps in-period GTV/CAC is higher in 2H because 2H typically sees more family holidays like Thanksgiving or Christmas where families might have to buy groceries in bulk and willing to try delivery. Might be a bit anecdotal but either way, I’m going to model 2H to have a better in-period GTV/CAC to follow the 2022 pattern.

So, what to make of this then? Like I mentioned last post, the bulls will say that 1H23 is experiencing macroeconomic headwinds so once we get through the cycle, the cohort GTV growth should recover. Bear will probably point to the more recent cohorts having greater declines and say that cohort quality deterioration is clear and that points to the limited TAM of those who are willing to actually pay up for grocery delivery. Until we get through the cycle, it’s hard to believe the bulls, so in the near-term, I’m going to say the bears have the upper hand.

From my modeling perspective, I feel like the important questions are 1) what does in-period GTV/CAC look like going forward? and 2) what are new cohort GTV growth curves? For (1), if you don’t want to use the in-period GTV/CAC, that’s fine, I’m just asking what CAC dynamics are going to look like going forward.

Projections

Based on in-period GTV/CAC trends and cohort dynamics, I’ve laid out a few cases for GTV projections:

In the base case, I’ve assumed the following:

All future cohorts to see a year-1 pop followed by growth rates decelerating by 2/3 and a steady state of 2-3% growth

The 2022 cohort growth of 30% in 2023 falling from 1H23’s growth of 54%

2023-2026 cohorts’s year-1 pop to decelerate by 5% every year

In-period GTV/CAC steady at 2023’s rate of 3.0x

To illustrate, here is the cohort waterfall I’ve modeled in the base case:

Below I’ve constructed a GTV growth bridge to tease out the impact of the 2020 cohort over time. I’ve also broken out this “new cohort year-1 pop”, which is just the idea that new cohorts see a net GTV bump in the first year post acquisition. The remaining contribution is either from newly acquired customers or the steady state of prior customers.

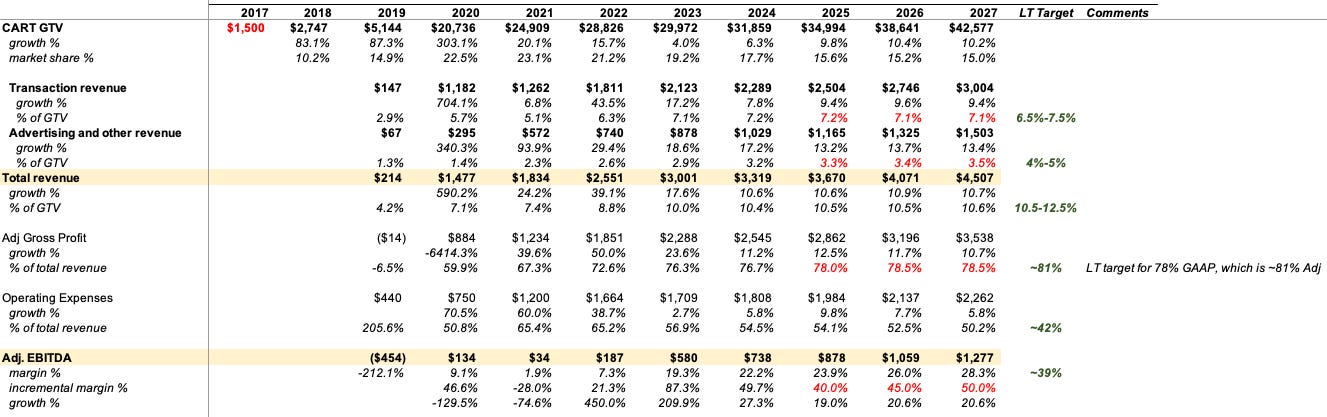

Management provided LT Targets in its IPO deck, pointing to ~39% EBITDA margin vs 2022’s 7.3%. Below is the base case numbers compared to the provided LT targets.

Some comments on the LT Targets:

LT transaction revenue target of 6.5%-7.5% is a bit disappointing given that 1H23 came in at 7.2% implying minimal upside and some downside to that take rate. I think this reflects our prior discussion on grocer concentration and CART’s likely inability to take up retailer fees over time.

LT advertising take rate of 4%-5% was higher than I anticipated. With grocer EBIT margins at a thin 1-3% of sales, I’d expect slotting fees to be at most 2-3% (i.e. grocery stores breakeven to maybe slightly positive on grocery item sales and make the rest the profits on slotting fees) but I suppose with the infinite canvas of the internet, you’re able to expand the effectiveness of advertising fees - i.e. every shelf is the eye-level one when you’re viewing it through the app.

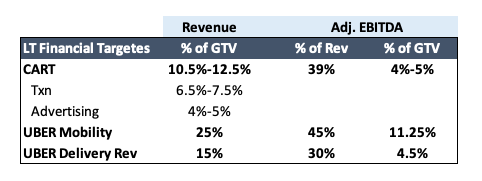

LT EBITDA margins of 39% feels reasonable compared to UBER’s LT Delivery EBITDA margins of 30%. On a % of GTV, the two are similar. See below for a comparison between CART and UBER’s LT financial targets.

I always imagined that grocery delivery might yield a greater profit margin than food delivery because you can carry greater GTV per trip as 1) grocery basket sizes are higher and 2) you don’t really need grocery to be delivered within 30-60 minutes, unlike food which needs to be hot and ready, so you’d imagine route density to be better for grocery since you have more time to plan + more deliveries per trip.

I suppose the benefits there are offset by grocer concentration pushing down retailer fees, which we can see in the rev as % of GTV being lower for CART.

On the other hand, advertising revenues of 4%-5% should be pretty high margin (maybe 70%-80% gross profit?) and I don’t think UBER Delivery benefits from the save revenue mix of advertising fees so on net I would have expected grocery Adj. EBITDA as % of GTV to still be higher than UBER Delivery.

Maybe it’s a conservative target or perhaps the UBER Delivery margins are aspiration (probably the latter given CART’s degree of profitability vs UBER at the moment).

Valuation

On Monday, CART updated its S-1 to indicate an IPO price range of $26 to $28 per share. Based on the outstanding common shares, the newly issued shares, and the additional dilution from options, RSUs, and the Series A preferred, we’re looking at ~331m outstanding diluted shares for valuation purposes, putting us at ~$8.6B to $9.3B. See below for share count calculations.

As many have noted, this is a significant drop from the $39B valuation round set in 2021 but you know, DASH is down (-66%) from its peak and ABNB is down (-31%) for comparison. With PF cash of nearly $2B and effectively no debt, we’re looking at an EV of ~$7B.

Compared to peers, the valuation (at the IPO midpoint of $27/share) is definitely cheaper than gig-economy peers at ~9.5x FY24 EBITDA compared to an average of ~18x. On a EV/sales basis, I’m seeing ~2x vs average of ~3x.

Investment Positives:

Category leader in a large TAM opportunity that’s only 12% penetrated.

Room for advertising fee growth to 4-5% of GTV, which is higher margin.

2022 cohorts seeing growth in 1H23, potentially getting past the impact of COVID-driven customers, so a case could be made for improving cohort dynamics going forward.

Cheaper than peers but also noting the slower growth.

Investment Negatives:

Grocer concentration to pressure any upside to transaction revenue take rates and poses tail risk if one of these guys go in-house or partner with a competitor.

New cohort performance getting worse.

End market doesn’t grow and it’s unclear how many people are willing to may a premium for grocery delivery, especially as the risk of recession hangs over the consumer.

Competition from DASH, UBER, AMZN, and grocer white-label initiatives.

Thoughts on selection growth constraints: people have noted that these platform see increased engagement when selection improves (i.e. more restaurants on UberEats = more usage) and due to the concentration of grocers in the US, there’s little room for greater selection on CART. I’m not sure I agree that CART needs this; I like a greater selection of restaurants on my food delivery app because, well I want a greater selection of food - for groceries, since the largest grocers carry most of the commonly used SKUs and produce anyways, I’m not sure whether adding another supermarket with similar if not the same selection will entice me to use it more. That said, I think the issue here is exactly that most grocers offer similar SKUs - I’m willing to pay up for food delivery because the food options in a radius of my walkable distance is narrow so I’m getting more selection from a delivery app whereas if there’s a grocery store that’s walkable or a 10min drive from me, adding another store isn’t going to interest me much.

If there’s anything you think I got wrong or that you disagree on, please comment or message me!